Financial Assistance for Home Care of Elderly Loved Ones

Financial Assistance for Home Care of Elderly Loved Ones

Financial assistance for elderly home care is defined as government-funded subsidies, Medicaid programs, and veteran benefits that reduce or eliminate out-of-pocket costs for in-home care services. Medicaid alone covers over 5 million older adults annually through its Home and Community-Based Services programs, making it the single largest source of senior care funding options in the United States. Beyond Medicaid, programs like the VA’s caregiver stipend and state-specific subsidies such as Florida’s Home Care for the Elderly give families real, accessible paths to affordable care. This guide breaks down every major program, who qualifies, and exactly how to apply so you can stop guessing and start acting.

What types of financial assistance are available for elderly home care?

Financial aid for home care falls into four main categories: federal Medicaid programs, state-specific subsidies, veteran caregiver benefits, and supplemental utility assistance. Each category covers different services and carries different eligibility rules, so knowing the full picture before you apply saves significant time.

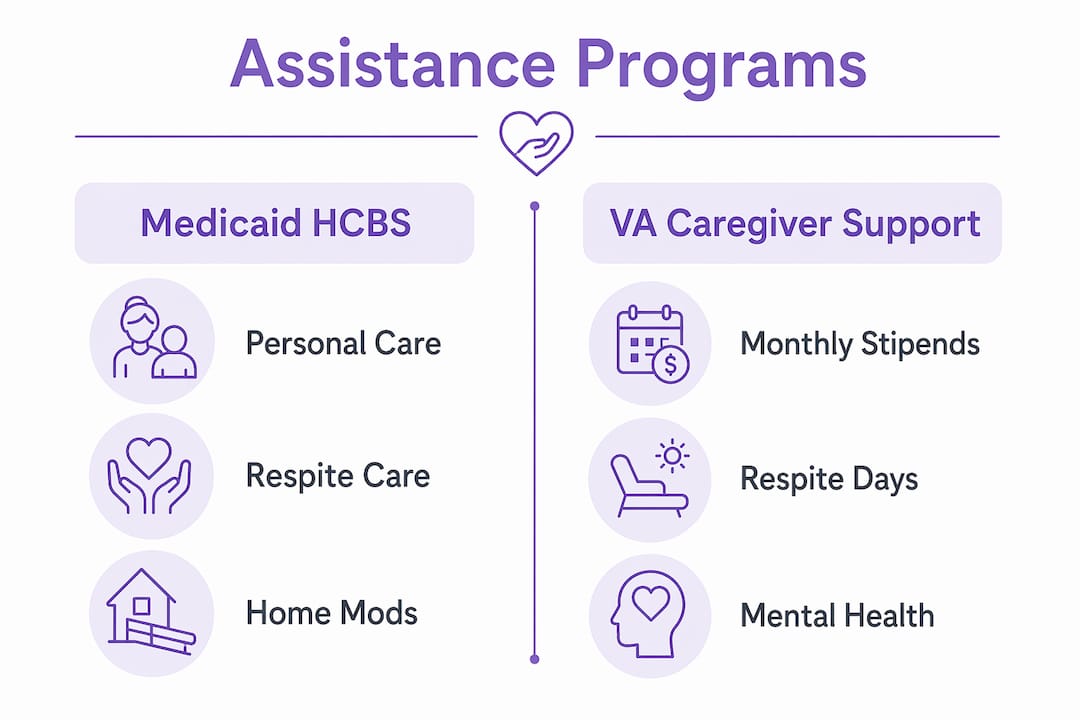

Medicaid home and community-based services

Medicaid’s HCBS programs are the backbone of government assistance for elderly care. Covered services include personal care, adult day care, respite care, home modifications, and in many states, direct payments to family caregivers. States design their own HCBS waivers under federal guidelines, which is why a program in Texas looks different from one in Maine. State Medicaid HCBS waivers define covered services and eligibility locally, so your first call should always be to your state Medicaid office.

One feature families often overlook is self-direction. All states with self-directed care allow enrollees to select, train, and dismiss their own caregivers, including family members. This means a daughter or son can legally be paid to care for a parent, which reduces both the financial and logistical burden on the household.

State-specific home care subsidies

Florida’s Home Care for the Elderly (HCE) program is one of the clearest examples of how states build on federal Medicaid funding. The HCE program provides a base subsidy of $160 per month plus additional allowances for specific items such as incontinence supplies, wheelchairs, and home health aides. That structure, a base cash grant plus targeted add-ons, is a model other states replicate in different forms. Families in Florida should map their loved one’s specific needs against the HCE’s covered categories to capture every dollar available.

VA caregiver support for veteran families

The VA’s Program of Comprehensive Assistance for Family Caregivers (PCAFC) is among the most generous caregiver support programs in the country. Eligible caregivers receive monthly stipend payments, more than 30 days of respite care annually, mental health counseling, and caregiver training. Payments are made via direct deposit after enrollment. The veteran must have a qualifying service-connected disability rating, and the caregiver must be a designated primary family caregiver to qualify.

Comparison of major assistance programs

| Program | What it covers | Who qualifies |

|---|---|---|

| Medicaid HCBS | Personal care, respite, home mods, caregiver pay | Low-income older adults meeting functional criteria |

| Florida HCE | $160/month base plus specific supply subsidies | Florida residents not in Medicaid-funded facilities |

| VA PCAFC | Monthly stipend, respite, training, counseling | Family caregivers of eligible veterans |

| LIHEAP | Utility bill assistance | Low-income households, income-tested |

Who qualifies for financial assistance and what are the eligibility requirements?

Eligibility for most home care subsidies for seniors depends on three factors: income, assets, and functional need. Meeting all three is required, and missing any one of them disqualifies an application regardless of how strong the others are.

Income and asset limits

For Medicaid’s non-MAGI pathways, which govern long-term care for older adults, income must fall below 300% of the SSI limit, which equals $2,982 per month for individuals in 2026. Asset limits are typically set at $2,000 for an individual, though some states allow slightly higher thresholds. Home equity rules vary by state but generally do not count the primary residence as an asset while the applicant lives there.

| Eligibility factor | Typical threshold | Notes |

|---|---|---|

| Monthly income | Up to $2,982 (300% SSI, 2026) | Varies by state; some states use different multipliers |

| Countable assets | Under $2,000 | Primary home usually excluded |

| Functional need | Difficulty with 2+ ADLs | Bathing, dressing, eating, mobility |

| Veteran disability | Service-connected rating required | VA PCAFC has specific rating thresholds |

Functional need assessments

Medicaid requires applicants to document functional limitations through an activities of daily living (ADL) assessment. ADL assessments focus on abilities like bathing, eating, dressing, and mobility. This step is critical and frequently underestimated. A caseworker or nurse typically conducts the assessment in person, and the results directly determine which services are authorized and at what level. Families should prepare a written log of daily care needs before the assessment to make sure nothing is missed.

Pro Tip: Document your loved one’s daily care needs in a written log for at least two weeks before the Medicaid ADL assessment. Caseworkers rely heavily on what they observe in a single visit, and a detailed log gives them the full picture.

State-by-state variation is significant. Some states have waiting lists for HCBS waivers that stretch months or years. Others have income disregard rules that allow higher earners to qualify through spend-down provisions. Reviewing your state’s specific Medicaid plan with a local Area Agency on Aging (AAA) is the fastest way to understand what applies to your situation. You can find state-specific qualification details through resources like the Helping-hands-home-care senior care guide.

How to apply for financial assistance for home care: step-by-step

Applying for elderly care financial help is a multi-step process that rewards preparation. Families who gather documentation before contacting agencies move through the system significantly faster than those who start without it.

-

Gather documentation first. Collect proof of income (Social Security award letters, pension statements), bank statements showing assets, identification, and any existing medical records documenting your loved one’s care needs. For veterans, gather the DD-214 discharge papers and VA disability rating letter.

-

Contact your local Area Agency on Aging. The AAA network, administered under the Older Americans Act, connects families to state and local programs including Medicaid waiver applications, meal delivery, and transportation. Find your local AAA through the Eldercare Locator at eldercare.acl.gov.

-

Apply for Medicaid HCBS. Submit your application through your state Medicaid office or Benefits.gov. Be explicit about functional limitations on the application. Incomplete functional information is the most common reason for delays or denials.

-

Request an ADL assessment. After your application is received, a state-assigned assessor will schedule an in-home visit. Use your written care log during this visit. The assessment outcome determines your service authorization level.

-

Understand waiver waiting lists. HCBS waiver availability varies by state, and some programs have waiting lists. Apply as early as possible. Being on a waiting list does not prevent you from accessing other programs in the meantime.

-

Enroll in VA caregiver programs if applicable. Apply through the VA’s Caregiver Support Program at caregiver.va.gov. Set up direct deposit during enrollment to avoid payment delays. The VA assigns a Caregiver Support Coordinator who guides families through the process.

-

Set up self-directed care if approved. If your state’s Medicaid program allows self-direction, you can hire a family member as a paid caregiver. Self-directed Medicaid care requires the enrollee or a designated representative to manage caregiver recruitment, scheduling, and dismissal. This is more administrative work but gives families maximum control.

Pro Tip: Apply for multiple programs simultaneously rather than waiting for one to be approved before starting another. Medicaid and VA programs operate independently, and there is no rule against receiving benefits from both if you qualify.

Understanding caregiver responsibilities and support structures before you start self-directing care will save you from administrative headaches later.

How to budget and plan financially for elderly home care with assistance

Budgeting for home care means combining multiple funding sources because no single program covers every expense. The goal is to map your loved one’s specific needs against available coverage categories and identify the gaps you will pay out of pocket.

Start by estimating the full cost of care. Home health aide services average between $25 and $35 per hour nationally, and non-medical personal care runs slightly less. Specialized services like skilled nursing or physical therapy cost more. Once you have a monthly cost estimate, subtract what each program covers to find your true out-of-pocket exposure.

Key budgeting considerations for families:

- Layer your funding sources. Medicaid HCBS may cover personal care hours while a state subsidy like Florida’s HCE covers supplies. LIHEAP utility assistance frees up household cash that can go toward care costs not covered by Medicaid.

- Account for subsidy structures. Programs like Florida’s HCE use a base grant plus specific subsidies for defined categories. Map your loved one’s needs to those categories before assuming full coverage.

- Budget for respite care. Caregiver burnout is a real financial risk. If a family caregiver stops providing care due to exhaustion, the cost of replacing them with a professional is substantial. VA PCAFC’s 30-plus days of annual respite is a direct financial offset for this risk.

- Plan for non-medical costs. Meal preparation, house cleaning, and transportation are often not covered by Medicaid but are real care expenses. Services like meal preparation support and home cleaning from providers like Helping-hands-home-care can fill these gaps affordably.

- Avoid the spend-down trap. Some families spend down assets to meet Medicaid’s $2,000 limit without realizing that certain asset transfers within five years can trigger Medicaid penalties. Consult a Medicaid planning attorney before making large transfers.

Families who treat financial planning for home care as an ongoing process rather than a one-time task consistently manage costs better. Reassess your funding mix every six months as care needs change.

Key takeaways

Families who apply early, document thoroughly, and layer multiple funding sources access the most financial assistance for elderly home care with the least delay.

| Point | Details |

|---|---|

| Medicaid HCBS is the primary source | Medicaid covers personal care, respite, and caregiver pay for over 5 million older adults annually. |

| State programs add targeted subsidies | Programs like Florida’s HCE provide a base monthly grant plus add-ons for specific care supplies. |

| Veterans have dedicated caregiver benefits | VA PCAFC offers monthly stipends, 30+ days respite, and training for qualifying family caregivers. |

| ADL documentation drives eligibility | A written daily care log prepared before the assessment strengthens Medicaid functional need evaluations. |

| Layer funding sources to close gaps | Combining Medicaid, state subsidies, and LIHEAP reduces out-of-pocket costs more than any single program alone. |

What I’ve learned navigating financial assistance for elderly families

The single biggest mistake I see families make is waiting until a crisis to start the application process. Medicaid HCBS waitlists in some states run six to eighteen months. By the time a family realizes their loved one needs daily care, they are already behind. The families who fare best start the paperwork the moment care needs become apparent, even if they are not sure they will qualify.

State variation in these programs is genuinely surprising, even to people who work in this space. Treating Medicaid as a starting point rather than a fixed rulebook is the right mindset. What is covered in one state may not exist in another, and the income rules that disqualify someone in one state may have a spend-down workaround in the next.

I also think the VA caregiver program is underutilized. Many veteran families do not know the PCAFC exists, and those who do often assume the disability rating threshold is too high. The respite care benefit alone, more than 30 days annually, has a real dollar value that most families never capture.

Finally, do not underestimate the value of caregiver training. The VA offers it as part of PCAFC, and some state programs include it as well. A trained family caregiver provides better care, lasts longer in the role, and reduces the likelihood of costly hospitalizations caused by preventable care errors. That is not a soft benefit. It is a financial one.

— Michael

How Helping-hands-home-care supports families navigating home care funding

Securing financial assistance is only half the equation. The other half is finding a care provider who delivers on the promise of quality in-home support.

Helping-hands-home-care works with families across the funding spectrum, whether you are using Medicaid HCBS, a VA stipend, or paying privately while you wait for approval. Our home health aide services are designed to complement what financial assistance programs cover, filling the gaps in personal care, meal preparation, and daily support. We also offer house cleaning and massage therapy for seniors who need more than medical care at home. If you are ready to pair your financial assistance with compassionate, reliable care, visit Helping-hands-home-care to learn how we can support your family.

FAQ

What does Medicaid cover for elderly home care?

Medicaid covers personal care, adult day care, respite care, home modifications, and in many states, payments to family caregivers through HCBS waiver programs. Coverage specifics vary by state, so contact your state Medicaid office for a full list of authorized services.

How much income can you have and still qualify for Medicaid home care?

In 2026, Medicaid’s non-MAGI income limit for older adults is generally $2,982 per month for individuals, which equals 300% of the SSI threshold. Asset limits are typically $2,000, though the primary residence is usually excluded from the asset count.

Can a family member be paid to provide home care?

Yes. Self-directed Medicaid programs in all participating states allow enrollees to hire, train, and pay family members as caregivers. The enrollee or a designated representative manages the caregiver relationship directly.

What financial help is available for veteran caregivers?

The VA’s PCAFC provides monthly stipends, more than 30 days of annual respite care, mental health counseling, and caregiver training to eligible family caregivers of veterans with qualifying service-connected disabilities. Apply through caregiver.va.gov and set up direct deposit during enrollment.

How do I find grants for elderly care services in my state?

Contact your local Area Agency on Aging through the Eldercare Locator at eldercare.acl.gov. AAAs connect families to state-funded grants, subsidies, and personal care assistance programs that vary by county and state. Applying to multiple programs simultaneously maximizes your chances of receiving support quickly.